The government scheme is reshaping how Australians buy their first home

Something significant happened when the 5% Deposit Scheme expanded last October. Loan volumes at participating lenders jumped 16.4% in just six months. Enquiries from Australians aged 18 to 35 surged by more than 20%. And 81.9% of first home buyers purchased outside their existing suburb suggesting that when the financial barrier drops, people stop waiting and start acting. That’s not a small shift. That’s a generation of buyers who had almost given up, finding a way in.

So what’s actually changed?

Normally, if you’re buying with less than a 20% deposit, lenders charge you Lenders Mortgage Insurance LMI for short. It’s an insurance policy that protects the lender, not you, and it can add anywhere from $8,000 to $30,000 or more to your costs, depending on the purchase price.

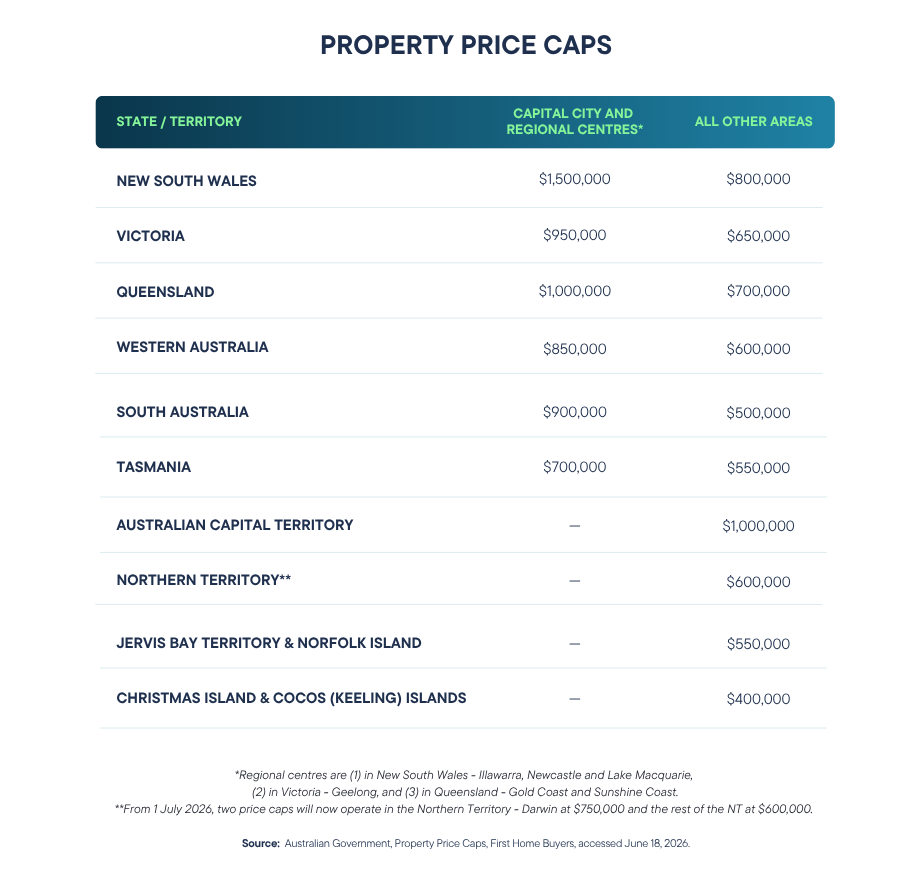

Under the 5% Deposit Scheme, the federal government guarantees part of your loan, which means eligible buyers can purchase with just a 5% deposit and pay zero LMI.

For a lot of people, that’s the difference between buying now and waiting another three to five years.

But it’s not the right fit for everyone

A smaller deposit means a larger loan. A larger loan means more interest paid over time and less equity in your corner early on. For some buyers, that trade-off makes complete sense. For others, a slightly different approach might put them in a stronger position long term.

That’s exactly the kind of conversation worth having before you commit to anything

.

Thinking about whether this could work for you?

I’m happy to walk you through it, no obligation, no pressure, just a straight answer based on your situation.