Negative Gearing Changes: Could Established Property Values Fall 5–10%?

Following the recent Budget announcements, I’ve been saying that established property values could decline by between 5% and 10%, and we’re now starting to see evidence that supports that view.

Recent data and market commentary are showing signs of weakness in investor-focused established property markets, while at the same time we’re seeing increased demand for new build investment properties and development sites.

The reason is relatively simple. Investors don’t just buy property based on location and growth potential. They also look at the after-tax return. When governments change tax settings, the market adjusts accordingly.

This raises an important question for the Australian property market:

If negative gearing benefits are reduced or removed for established properties, how much less will investors be willing to pay? And will that demand simply move into new housing instead?

Understanding the Value of Negative Gearing

Negative gearing has long been one of the key incentives available to Australian property investors.

For many investors, the ability to offset property losses against taxable income improves cash flow and helps justify paying a higher purchase price for an investment property.

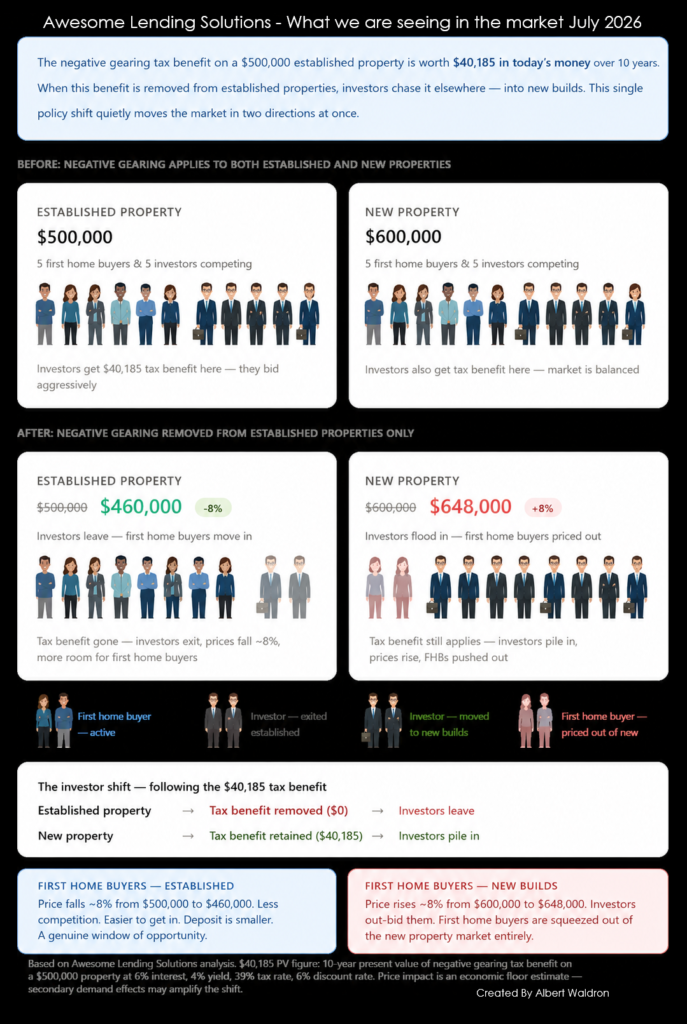

To understand the financial impact, we recently modelled the numbers on a $500,000 investment property.

Using conservative assumptions and analysing the benefit over a 10-year period, we found that the value of the negative gearing tax benefit equated to approximately $40,185 in today’s dollars.

That represents around 8% of the property’s value.

While every investor’s tax position will differ, the broader economic principle remains the same: when you remove a financial benefit, you reduce what buyers are willing to pay.

Why Established Property Values Could Fall

Property values are ultimately determined by supply, demand and purchasing power.

If investors lose a tax benefit worth approximately 8% of a property’s value, it is reasonable to expect that many would reduce their purchase price accordingly.

From a purely economic perspective, the logic is difficult to ignore.

Imagine two identical investment opportunities:

- One provides favourable tax treatment.

- The other does not.

- Both produce similar rental income and growth prospects.

Most investors will naturally place a higher value on the asset delivering the stronger after-tax return.

This is why I’ve consistently argued that established property values could face downward pressure if negative gearing changes are implemented.

Importantly, this isn’t just about the direct loss of tax benefits. It is also about what happens to overall market demand.

When investor demand declines, competition reduces. Fewer active buyers generally means lower price growth, longer selling periods and increased negotiation power for purchasers.

That’s where the potential 5% to 10% decline starts to become a realistic scenario rather than simply a theoretical discussion.

The Shift Towards New Build Investment Properties

Whenever governments change investment incentives, capital tends to move elsewhere.

That’s exactly what we’re starting to see now.

Many investors are increasingly targeting:

- New build investment properties

- Off-the-plan apartments

- Townhouse developments

- House and land packages

- Development sites

The reason is straightforward.

If tax incentives remain available for new housing while becoming less attractive for established housing, investors have a clear financial motivation to redirect their funds.

In other words, money doesn’t disappear from the market,it simply moves.

We’ve already seen examples of this occurring in other markets around the world whenever tax concessions are altered. Investors adapt quickly because their goal is to maximise returns while managing risk and cash flow.

As a result, developers may become the biggest beneficiaries of any policy changes that reduce demand for established homes.

Could New Build Prices Rise by 8%?

This is where things become particularly interesting.

If investors lose approximately 8% of value through reduced tax benefits on established properties, there is a strong argument that some or all of that value could be transferred into the new housing sector.

Think about it this way.

If an investor was previously willing to pay $500,000 for an established property because of the available tax benefits, and those benefits disappear, they may only be willing to pay $460,000 to $480,000.

However, if a new-build property still provides attractive tax advantages, that same investor may be willing to pay a premium to secure it.

As more investors compete for a limited supply of new housing stock, prices can rise.

The market effectively begins capitalising those tax benefits into purchase prices.

While it may not occur immediately, increased investor demand could place upward pressure on:

- New home prices

- Land values

- Development sites

- Construction-focused

- housing projects

The question is whether that increase will be enough to fully offset any decline in established housing values.

What This Means for Property Investors

For investors, the key lesson is that tax policy matters.

Many property decisions are based on future cash flow projections, borrowing capacity and expected after-tax returns.

If negative gearing settings change, investors will need to reassess:

- Property selection

- Expected yields

- Cash flow projections

- Long-term growth assumptions

- Overall property investment strategy

This doesn’t mean established property investment suddenly becomes a bad idea. High-quality locations with strong fundamentals will always attract buyers.

However, investors may become more selective and place greater emphasis on rental yields, scarcity and long-term capital growth rather than relying heavily on tax advantages.

My View

My view remains relatively simple.

If investors lose a benefit worth approximately 8% of a property’s value, it is reasonable to expect that established property prices could experience downward pressure.

At the same time, demand for new build investment properties and development opportunities is likely to increase, potentially pushing those prices higher.

The exact outcome will depend on investor behaviour, housing supply levels and broader economic conditions, but the underlying economics are difficult to ignore.

The next 12 to 24 months could provide one of the most fascinating case studies we’ve seen in the Australian residential property sector.

The real question is this:

Will investors simply pay less for established properties, or will the shift in demand drive a meaningful increase in new-build prices?

As always, I’d love to hear your thoughts.